Farewell, Dashdot: An Open Letter

In early 2019, Gabi and I started Dashdot with a grand ambition to "help 10 people make better property investing decisions".

A little over 7 years later, we're very proud to say that, along with a truly world class team of exceptional humans, we've helped over 1,800 everyday Australian families buy over 2,800 properties and generate over $540m in wealth.

But today, I'm writing to inform you, with deep, deep sadness and regret, that this journey is coming to an end.

As of Thursday 28th May, 2026, Dashdot will be entering into voluntary liquidation.

The incredibly unfortunate reality is that many people are going to be negatively impacted by this, and for those of you who are, I want to offer my most sincere, and most heartfelt apology.

Truly, I am sorry.

This is not an outcome that any of us wanted, expected, or accepted without a fight.

To help you understand how we got here, I'll offer some insights, not excuses.

As recently as the end of February, Dashdot was in great health.

As a company we were growing, profitable, and actively improving the client experience and client outcomes.

We were, on all fronts, making great progress on impact, and innovation, and on almost every business metric that matters, Dashdot was in great shape.

Unfortunately a sequence of events subsequently unfolded that caused that condition to become compromised.

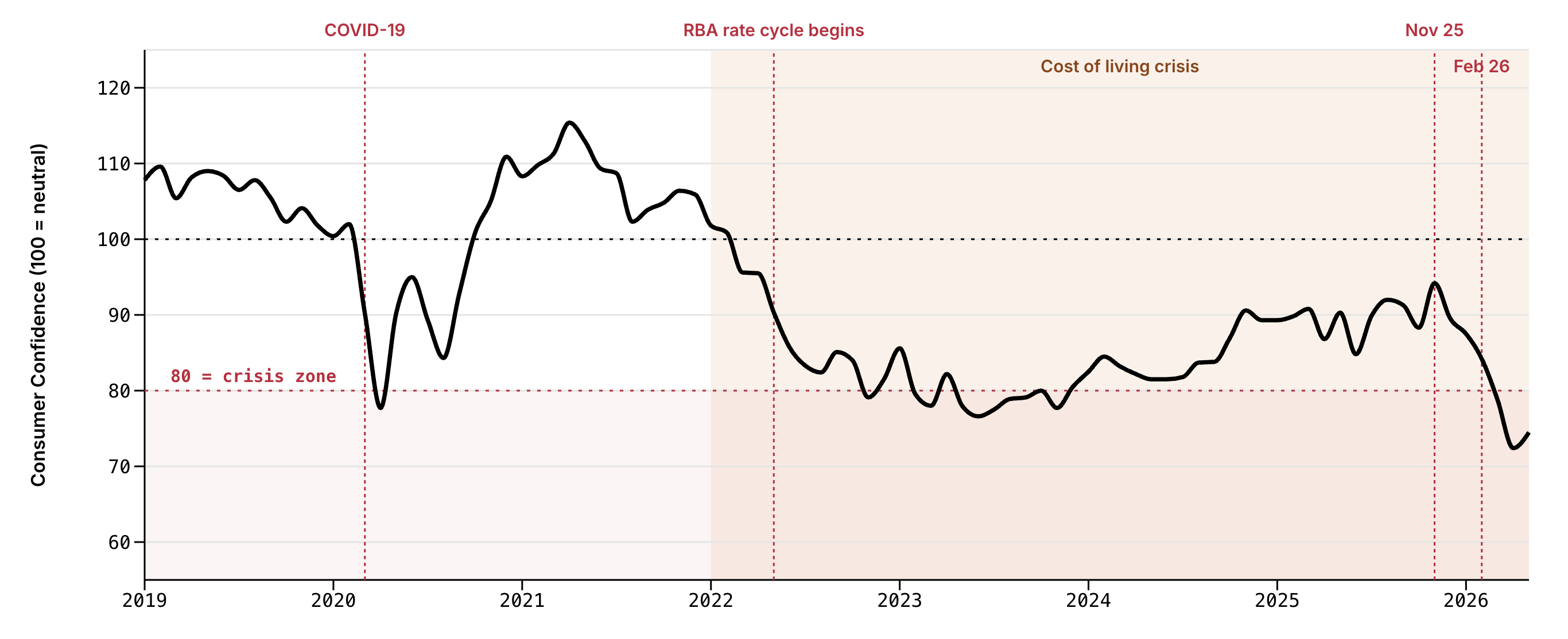

As a high level reference point, the external metric that has always mattered most to Dashdot over the last 7 years, has been Consumer Confidence.

As a consumer centred business, which relies on everyday Australians feeling confident about their current situation, particularly to the extent that they think and plan for the future, general consumer sentiment has always heavily influenced Dashdot's business dynamics.

Coming into 2026, Australian households were already deep in a sustained cost-of-living crisis that had been building since 2022, and had not eased.

- Inflation continued to push prices, and the cost of living, up throughout 2025.

- The Federal Energy Bill Relief Fund, which had been softening household power bills for two years, ended on 31 December 2025.

- Australia had been in a per capita recession for most of the prior two years, with real living standards going backwards.

- Housing affordability had continued to worsen across the same period.

- Nearly half of all Australians (48.7%) reported that cost-of-living pressures had triggered or worsened anxiety and depression. The figure was 72% for Gen Z.

- Cost of living was named by more than 1 in 3 voters as their single most important issue in the 2025 federal election, an unusually rare level of dominance for any single issue.

By any measure, Australians were already in crisis mode.

Then, from early February 2026, the conditions began to worsen.

Over the weeks and months that followed, three distinct forces converged on our business at the same time.

- A macro shock to an Australian economy that was already under sustained pressure.

- A policy shock to the property investment market we served.

- A platform shock to our primary client acquisition channel.

Each one alone would have been challenging.

Together, they broke the conditions our business depended on.

The first force was the macro cycle turning hard.

On 1 February 2026, APRA introduced Australia's first-ever formal cap on high debt-to-income lending. From that day, borrowing capacity for highly-leveraged buyers and investors began to tighten.

Two days later, on 3 February, the Reserve Bank raised the cash rate by 0.25% to 3.85%. The first increase in more than two years. The rate-cut cycle of 2025 was over.

Then on 28 February, coordinated strikes began in Iran. Within hours, the Strait of Hormuz was effectively blockaded. Global fuel prices spiked.

Petrol prices in Australia climbed week by week through March and April, peaking above $2.50 per litre. Trucking, freight, and a long tail of consumer goods got more expensive in lockstep.

But beyond the cost itself, the fear of an actual fuel shortage became part of the household conversation. The spectre of running out, on top of the price at the pump, was its own force on consumer sentiment, separate from the financial hit, and arguably as large as it.

The effect on Consumer Confidence was severe and immediate.

The ANZ-Roy Morgan Consumer Confidence Index fell from 77.8 in February to 66.0 in March. That is an 11.8-point single-month drop, the largest since the start of COVID in March 2020.

In the week of 23 to 29 March, the weekly reading hit 58.8.

That is the lowest Consumer Confidence reading in more than 50 years of measurement, surpassed only by a single weekend in Australian history: the COVID lockdown weekend of 28-29 March 2020.

And unlike that single weekend in 2020, this collapse has not eased.

The index has now been below 70 for 11 consecutive weeks, averaging 64.8 across that period. As of the most recent weekly reading, Consumer Confidence sits at 66.1. That is the eighth-lowest reading in 50+ years of measurement.

Six of the seven lowest readings ever recorded all came in the six weeks following the March collapse.

This is not a spike. This is a sustained collapse. It is the deepest and most sustained consumer confidence crisis in more than 50 years of Australian measurement.

On 17 March, the RBA raised the cash rate again, to 4.10%. On 5 May, they raised again, to 4.35%. By March, annual inflation had reached 4.6%, nearly double the 1.9% recorded just nine months earlier.

Mortgage stress moved with it. In January 2026, Roy Morgan classified 23.9% of Australian mortgage holders as 'at risk' of stress. By April that had climbed to 28.2%, or 1.47 million Australian households.

For context: during the worst weeks of the COVID-19 pandemic, with JobKeeper, JobSeeker, and mortgage holidays in place, that same figure was 17% to 20%.

Mortgage stress today is 35% to 40% worse than peak COVID, with no government support package this time around, and the RBA hiking rates rather than cutting them.

At the same time, real unemployment (Roy Morgan's broader measure that includes those who want work but haven't been able to find it) climbed to 10.1% in April 2026, equivalent to 1.63 million Australians. The combined measure of unemployed plus underemployed reached 20.9% of the workforce, or 3.38 million people.

By late April, Roy Morgan Business Confidence had collapsed 14.2 points in a single month, to 76.5. A new all-time record low. That is 0.4 points below the previous record set in April 2020.

61.3% of Australian businesses now expect 'bad times' for the economy over the next 12 months.

In short:

- Consumer Confidence at its lowest sustained level in over 50 years of measurement

- Business Confidence at an all-time low

- Mortgage stress 35-40% worse than peak COVID, with no government support

- Real unemployment at 10.1% (1.63 million Australians); combined labour underutilisation at 20.9%

- Annual inflation nearly doubled in nine months

- The RBA hiking three times in three months

- Petrol up 30-50%, with the fear of shortage compounding the cost

This is the environment Dashdot was trying to find, advise, and serve clients in.

The second force was the Federal Budget of 12 May 2026.

Its impact on our business, however, did not begin on 12 May.

From March 2026, media speculation about major changes to Australian property taxation had been building.

Industry commentary intensified week by week.

Conflicting reports about what was coming, how aggressive the changes would be, and which investors would be caught, ran through the property press for weeks.

By the time the budget itself was delivered, the property investment market had been absorbing sustained uncertainty for over two months, and the damage to investor sentiment was already well under way.

The Albanese government's fourth federal budget delivered the most significant changes to Australian property taxation in nearly three decades.

The two changes that mattered for our industry were:

- The 50% capital gains tax discount, in place since 1999, is to be replaced from 1 July 2027 with cost-base indexation plus a 30% minimum tax rate on real capital gains.

- Negative gearing on residential investment property is to be limited to newly-built dwellings only, with established properties purchased after 7:30 PM on 12 May 2026 caught by the new rules.

For nearly thirty years, the architecture of Australian property investing had rested on two assumptions: that capital gains would be taxed at half the marginal rate, and that the cost of holding an investment property could be offset against salary income.

The May 12 budget removed both for future investors.

Public commentary fractured immediately. Headlines warned of "the end of property investment." Forums filled with confused investors. The investor segment of the Australian property market entered a state of paralysis within 24 hours.

This was the first direct, policy-driven blow to investor confidence in the entire cycle.

Every prior pressure had been macro. This one was aimed directly at the people we worked with.

Then, within days, the downstream impact arrived.

On Friday 15 May, Westpac quietly told mortgage brokers not to count on future negative gearing when assessing investor serviceability.

On Monday 18 May, Macquarie Bank formally issued the first complete policy. From that date, Macquarie's investor lending calculator no longer included any add-back for the tax benefit of negative gearing on any post-budget purchase of an established property.

The bank also began triggering mandatory reassessment of existing investor pre-approvals.

CBA, NAB, and ANZ all moved to active review.

For a typical investor (a single applicant on $100,000 income with no existing debt), borrowing capacity fell by approximately 20% overnight, from $750,000 to $600,000, with no change to income, expenses, or interest rates.

For more highly-leveraged scenarios, the reduction was 25% to 33%.

Some pre-approvals issued only weeks earlier became unreliable overnight.

New investor enquiry slowed. Existing client conversations shifted from "when do we buy" to "what does this mean for me?"

In short:

- Two major tax policy positions, with direct impact on property investors, were removed for future investors

- Banks moved within days to strip the corresponding tax benefit from their lending calculators

- Investor borrowing capacity fell 20-33% overnight

- The market we served entered a state of paralysis

The third force was something almost no one outside the digital marketing world was watching.

Between early March and late April 2026, Meta's advertising platform, through which we acquired the great majority of our new clients, underwent significant changes.

Andromeda, Meta's new AI-driven ad system, reached full global deployment. The traditional methods of audience targeting that businesses like ours had relied on for years no longer worked the way they used to.

A separate delivery system update in early March pushed cost-per-thousand-impressions up significantly across consumer-facing accounts globally.

For Dashdot specifically, the combined effect was severe.

Our cost to acquire a new client roughly doubled in a matter of weeks. Our advertising-driven revenue more than halved over the same period.

And since the start of May, that revenue has fallen drastically further.

The Meta changes affected digital advertisers in a broad range of industries.

For Dashdot, they hit asymmetrically hard, not because the changes themselves were beyond our ability to adapt to, but because they landed at the precise moment our target market was being paralysed by the budget shock and consumer demand was being crushed by the macro cycle.

The Meta changes alone were absorbable.

The combination of the Meta changes with the other two forces was not.

In short: paid advertising on Meta became completely untenable and unviable, to the point that we could no longer continue running it. Our primary source of new client acquisitions was effectively cut off, at the same time everything else was breaking.

To summarise what hit our business between early February and late May 2026:

Force 1: The macro cycle turned

- APRA introduced Australia's first cap on high-DTI lending

- The RBA hiked the cash rate three times (to 4.35%)

- An oil and gas shock from the Iran conflict pushed petrol prices above $2.50 per litre, with the fear of shortage compounding the cost

- Consumer Confidence collapsed to its lowest sustained reading in 50+ years

- Business Confidence collapsed to an all-time low, lower than April 2020

- Mortgage stress rose to 35-40% worse than peak COVID, with no government support

- Real unemployment hit 10.1%; combined labour underutilisation hit 20.9%

- Annual inflation nearly doubled in nine months

Force 2: The Federal Budget directly hit investor confidence

- The 50% CGT discount removed for future investors

- Negative gearing limited to new builds only

- Banks stripped negative gearing benefits from their lending calculators within 6 days

- Investor borrowing capacity fell 20-33% overnight

- The investor segment entered a state of paralysis

Force 3: Meta's advertising platform broke our acquisition engine

- Our cost to acquire a new client roughly doubled

- Our advertising-driven revenue more than halved

- Revenue then fell drastically further from the start of May

None of these three forces were unique to Dashdot. Every property advisory in Australia faced the first two. Every business that depended on paid social media advertising faced the third.

But they hit us at the same time, in the same compressed window.

Each one alone would have been a significant challenge.

The combination was something we could not absorb.

Whilst the forces we faced were undeniable, it would be irresponsible of me to not take ownership.

For all of the external pressures, there are things that, in hindsight, we could have done to prevent ourselves from ending up here.

- Our marketing engine was too reliant on paid advertising.

- Our balance sheet wasn't robust enough to withstand external shocks of this magnitude.

These were the result of choices that we made over the years. They created fragilities that meant Dashdot started to break under the weight and pressure of these external factors.

The balance sheet fragility was, in part, a byproduct of continual reinvestment into the business to help more of our clients build stronger portfolios. We accepted a thinner buffer in exchange for greater impact. The conditions of 2026 revealed the cost of that trade-off.

With hindsight, there are always decisions you could have made differently. But I maintain that we always made the best decisions we could with the information we had at the time, and with a consistent commitment to our clients.

That said, I don't think anyone could have predicted the catastrophic sequence of events that unfolded for our business over the past few months.

And, of course, we weren't idle passengers watching all of this happen to us.

At the start of March, recognising the risks on the horizon, we instigated a process with our Corporate Advisory partners to do an equity raise to recapitalise the balance sheet.

By early April, business conditions had deteriorated so quickly that it became unfeasible to find investors who wanted to participate in the round.

We expended significant effort over these months to reduce our expenses. We lowered advertising and marketing costs. We reduced operational expenses to get as lean as possible. We did everything we could to lower our cost base without compromising the business.

Unfortunately, that wasn't enough.

Last week on Tuesday 19th May we made over 40 people redundant from Dashdot, which was necessary, but frankly, heartbreaking.

To every team member affected, those made redundant last week, and those of you still standing alongside the business today:

Firstly, thank you. You poured yourselves into building something we all believed in, and for that I will always be grateful.

Secondly, I am sorry. You deserved more than this. You gave everything you had to this business. I am sorry beyond words that we could not carry it further for you.

Across the weeks and months leading to today, we maintained a measured view that we would be able to find a path through, which is why we continued to press on.

In parallel, we also began exploring conversations with other companies in the space to potentially create an alternative pathway, through a merger, sale, or acquisition, that would let us ensure continuity and the best possible care for our clients.

Some of those conversations have significantly progressed and remain ongoing.

Whilst they are still in progress, we are not in a position to comment on these further at this time.

Over the past few weeks, on a daily basis, we assessed Dashdot's position, our prospects, and our potential to trade through. Each day, we judged that the best outcome for our clients and key stakeholders was to keep pushing forward.

That assessment has now changed.

Even with the best laid plans, and even with our best efforts, we have not yet been able to find a path forward that would let Dashdot continue as it stands.

Right now, we are about to hand control of Dashdot over to a liquidator. At that point, we will no longer be in control of the company.

We will, however, continue to do everything in our power, within the limitations we find ourselves in, to find a path forward for our clients.

From this point forward, there will be a limit to what I and the rest of the Dashdot team can say publicly.

Once the formal liquidation process begins, we are unable to comment on this situation publicly until that process is complete.

I want to be very clear: this is not our choice. This is not us hiding. It is a legal and practical constraint of the liquidation process itself.

I understand how frustrating that silence will be for the people most affected, and I am sorry for that frustration too.

We will provide further updates through the formal channels if and when we are able to.

To our clients, especially those who placed your trust in us with your wealth, your future, and your family's security: I am so sorry.

You did not pay us to receive a letter like this. You paid us to deliver on what we promised, and to be there for the long journey of building real wealth beside you.

The fact that we have been unable to do that, and particularly for any of you whose work with us is currently still in active progress, is the single thing that hurts most about this whole situation.

I am deeply, deeply sorry.

To our shareholders, and investors who supported us along this journey: I am also deeply sorry. You placed real trust in us, and that trust has not delivered the outcome that any of us hoped for. I am sorry that we didn't achieve all that we set out to.

All Gabi and I have ever wanted to do with this business is to serve, and to have a positive impact on the lives of the people we serve.

Again, to all who are affected, I'm truly, truly sorry that this is happening to you.

And, I hope this goes without saying, but for the avoidance of doubt: this situation has, and will continue to have, a significant material impact on Gabi and I as well.

I don't say that to ask for pity, not at all.

I say it because I want you to know we are in this too. Everything we've built for the last 7 years, and our continual reinvestment into the company to create better outcomes for our clients, is now, for all intents and purposes, gone.

I know that a lot of people will read this.

I know that a lot of people will be angry. I know that a lot of people will be upset. I know that a lot of people will cast judgement.

However you feel about this is absolutely fine.

I understand all of it, and I accept all of it. I am not going to ask anyone to feel anything other than what they feel.

The only thing I would ask, if you can find your way there, is for understanding.

We did our best. We always tried to put our clients first. And we faced the hardest conditions any of us had ever traded through, with everything we had.

For everyone impacted by this, I am deeply and unreservedly sorry.

We built Dashdot because we wanted to create a long, lasting, and positive impact on the world. We carried it as far as we could.

I am sorry that we could not carry it further.

Goose McGrath

Co-Founder, Dashdot