Navigating High-Interest Markets and Its Impact on Property Investors

Executive Summary

Dear Ambitious Investor,

If you’re like most property investors right now, you probably have your head in a spin.

Rising interest rates, talk of market crashes and more can make even the most stoic of investors start to get a little weak at the knees.

In this report, we’re going to tackle a few key topics, to empower you to make informed, intelligent property decisions.

Topics such as:

What happens to property investors when interest rates rise? Is property investing still affordable?

Is the property market going to crash?

Is all the growth over?

And more…

Sound good?

Ok, let’s jump in…

What Happens to Property Investors When Interest Rates Rise?

There are two great myths surrounding property investing and interest rates:

That rising interest rates cause house prices to drop

That rising interest rates make property investing unaffordable

However, history has debunked both these myths.

Consider the below data in relation to the claim that prices drop when interest rates are high…

1988 – 1989

Interest rates rose from 14% – 17% House prices rose by over 35%

1990 – 1993

Interest rates dropped from 17% – 9% That is an 8% drop in 3 years!

House prices did… not much

1994

Interest rates rose by almost 2%

House prices continued to drift upward

1996 – 1997

Interest rates dropped by nearly 4% House prices rose by almost 10%

Interest rates vs House prices 1986 – 1997

As can be seen on the graph, interest rates rose by 14% to 17% from 1988 to 1999. Over the same period, however, house prices rose by more than 35%.

From 1990 to 1993, interest rates had an 8% free fall, going from 17% to 9%. Meanwhile, house prices practically went flat. This, despite the corollary claim that when interest rates go down, prices should effectively go up.

Finally, interest rates fluctuated wildly from 1994 to 1997—first rising by almost 2% before dropping nearly 4%. Through it all, house prices only continued to drift upward.

What these data points suggest is that interest rates and property prices follow individual trends that do not indicate any causation or correlation. As interest rates fluctuate, property prices remain fixed on their growth trajectory.

Now, let’s get a bit more technical by looking at the relationship between interest rates and median sales price growth (MSPG).

Fixed Term Interest Rates vs 1 Year MSPG

2-month median house price growth

2-month median house price growth

in both capital cities and regional areas for all of Australia, compared to the average fixed term mortgage interest rate.

Note: Each of those coloured lines represents a different market, either capital

or regional, by state.

What you’re looking at is a graph of the 12-month MSPG in both capital cities and regional areas of Australia (indicated by the grey lines), compared to the average fixed term mortgage interest rate (the red line) from 1993 to today.

Some important data points to consider:

Between April 2001 and December 2003, interest rates rose from 6% to 7%. Yet, property markets grew by record amounts.

Between December 2003 to July 2008, interest rates rose from 6.5% to 9%. Still, property markets continued their growth.

Between March and October 2009, there was a 2% rate rise in just seven months. At the same time, growth skyrocketed.

Most interestingly, however, is what that black box at the bottom of the graph indicates. It shows all the times growth went negative. Notice how it only happened when interest rates were declining. While the rest of the time, markets were still growing.

All these trends point to one fact:

that interest rates and property prices are unrelated.

This effectively debunks the first myth – that high-interest rates might be causing property prices to freefall soon.

Let’s now turn to the second myth.

Is Property Still Affordable?

The assumption is that it becomes unaffordable to be a property investor when interest rates rise. To a certain degree, interest rates do affect affordability, but primarily as far as new homeowners go.

Consider that someone who already owns a home is unlikely to be priced out of their ownership because they’re already being assessed at 3% higher than their repayments.

Where the squeeze happens is when new entrants try to penetrate the market. That’s where it gets a bit more challenging. After all, higher interest rates also mean buffer rates and financial risk assessment rates go up, making it harder for new homeowners to get into the market.

As new homeowner affordability worsens, fewer people are able to buy their first home, which means that they stay in the “renter pool”, whilst at the same time, more young adults are entering into the rental pool as they come of age and seek independence.

This increases demand for rentals, at a time when there are very new rental properties becoming available on the market.

That’s why in most cases, when interest rates go up, rents likewise go up. However, when interest rates go down, most of the time, the rent stays the same. And often, rents even continue to go up, albeit at a slower rate.

This is good news for property investors, but the question is… Why?

Well, that is because of the rental crisis in Australia.

There just aren’t enough houses for people who want to buy them. Thus, even if interest rates go down and homeowner affordability goes up, all it does is push the supply of rentals down, once again pushing prices up.

As a result, most rents across the country have been growing by 10% to 20% annually for the past couple of years.

Still, not all locations are created equal. This means the issue of affordability may only be answered on a case-to-case basis. After all, affordability is inherently tied to profitability. And profitability relies on investing in the right property at the right place at the right time.

This is not an easy metric to gauge, which is why Dashdot designed an Investor Affordability Ratio.

We use this custom ratio to identify locations that are still affordable for property investors. And we do this by looking at the ratio of monthly rent divided by the average monthly mortgage repayment in that area.

To illustrate, consider the two graphs below.

Investor Affordability Ratio → North Bondi, NSW

(Monthly Asking Rent / Monthly Mortgage Repayment)

What you see above is the investor affordability ratio in North Bondi. It’s all in the red, which means it’s now a very unaffordable suburb. Investors who buy properties in the area are thus buying at a negative profitability position.

What you see above is the investor affordability ratio in North Bondi. It’s all in the red, which means it’s now a very unaffordable suburb. Investors who buy properties in the area are thus buying at a negative profitability position.

Even if rents rise in North Bondi, property investors in the area would have a long way to go before they can dig themselves out of the red.

Investor Affordability Ratio → Dashdot Location B

(Monthly Asking Rent / Monthly Mortgage Repayment)

In comparison, illustrated above is an undisclosed location we’ve discovered for our clients. Using the investor affordability ratio, we were able to direct our clients to this location where they are able to buy properties that are profitable from day one.

In comparison, illustrated above is an undisclosed location we’ve discovered for our clients. Using the investor affordability ratio, we were able to direct our clients to this location where they are able to buy properties that are profitable from day one.

After locking in their prices on day one, investors in this area get to enjoy strongly rising rents, year after year, meaning they’re going from strength to strength.

As opposed to North Bondi, which, even with strong rental growth, would have a long way to go before it becomes profitable.

Not only that, the undisclosed location that is currently “in the green” is also a high growth location, having experienced over 19.7% growth in the last 12 months.

This is a perfect illustration that across-board affordability is not defined by interest rates. Again, the issue can only be solved by looking at the nuances of each location and using the investor affordability ratio to determine whether or not a certain location is still affordable and profitable.

Bottomline: property investing can still be affordable. In fact, investors can start with as little as$50K to $60K capital.

Take the case of Toni and Rosie, for instance.

Toni & Rosie: Business Owner Couple 3 properties in 9 months!

Started with $60,000

To be fair, Toni and Rosie did leverage equity from another property. But that doesn’t change the fact that they started investing with just $60,000 cash at hand.

To be fair, Toni and Rosie did leverage equity from another property. But that doesn’t change the fact that they started investing with just $60,000 cash at hand.

Summarised in the image above are the investments they were able to secure with the capital they had. As you can see, the couple’s first investment delivered a 219.2% ROI in just under two years. The second property gave them 51.5% ROI, and the third one, 156.4%.

What these numbers don’t reflect, however, is the massive change that property investing has brought to Toni and Rosie’s lives. Apart from improving their financial position, property investing has likewise shifted their emotional position to positive.

They have since moved to Surfers’ Paradise to live near the beach. They’ve had their first child. And through these life-changing decisions, Toni and Rosie still feel safe and secure, all because their property portfolio set them up for long-term success in a massive way.

Toni and Rosie’s story is just one of many, many case studies proving that property investing can still be affordable, so long as the investor is equipped with the right tools and know-how to navigate all types of markets, especially high-interest environments.

Is the Market Due for a Crash?

With the issue of high-interest rates and its (non)-impact on property prices and investor affordability all settled, let’s move on to yet another controversial topic:

The supposed impending crash of Australia’s property market.

News of an impending crash has been around for quite a while now. It has made tons of interested property investors fearful to make a move, while others are convinced about a looming fire sale where heaps of people would be selling their homes for lower prices. However, this is not a strategy that Dashdot agrees with—for the simple reason that we don’t believe a crash will happen any time in the foreseeable future.

We have three reasons for thinking this way:

1.Borrowing is pressure-tested.

Everyone’s ability to borrow on a property located in Australia is pressure-tested at 2%-3% higher than what the actual interest rate is.

Take, for instance, the alarmist view that interest rates will go up at 3%. On the off chance that these projections come to fruition, a fire sale just wouldn’t follow suit. It’s unlikely that people will suddenly go underwater in repayments because they’re pressure-tested against such rates anyway.

Additionally, we don’t see people compromising on a need as basic as housing. Repayments would still be on top of their priority lists, which means a fire sale is very unlikely to happen.

2. Real estate does not behave the same way as the financial market.

With both the share market crashed in, many people have come to the conclusion that it’s only a matter of time before the real estate market follows suit. However, this couldn’t be farther from the truth.

The main reason businesses may have become unprofitable and unattractive to investors is inflation. The increasing prices of goods and services are pushing up the cost of operating a business, thus squeezing the profit margins of investors. This is why the share market is performing poorly.

On the other hand, inflation is a godsend for residential property values because there’s a finite supply but high demand for property. This is exactly why real estate investing has long been considered a hedge against inflation.

Overall, the real estate market and the financial market have fundamentally different drivers. Thus, trying to predict the future of the property market based on what has been happening in the share market is akin to predicting the price of apples by analysing oranges.

3. Past performance does not indicate future performance.

Anyone who projects a property market crash is looking to the past to try and tell what’s going to happen in the future. Our view is that this is a fool’s errand, considering that past performance does not indicate future performance when it comes to property.

In the 1980s, for instance, people were already saying the same things: that house prices can’t keep going up. And that people can’t afford to keep paying them, so property prices won’t keep doubling.

But here we are.

In the end, the key thing to examine is not whether a crash is looming. Instead, it’s whether or not there is still growth to be enjoyed for players who are not yet in the market. Or even those who have yet to get sufficient returns from their investment.

Is the Growth Period Over?

Aaron & Kira: Proof that areas are still booming

Aaron & Kira: Proof that areas are still booming

Since there are 15,264 towns and suburbs in Australia, it means one thing:

There will always be areas that are growing and areas that are slowing.

At first, Aaron and Kira did not believe this. Like many property investors who weren’t able to get an early start on real estate, they thought the growth period was over.

Luckily, they took the leap of faith and made their first investment just three months prior to writing time. And since then, their property’s value has already grown by 15.2%. Taking a look at the summary of their investment above, you’d see that it translated to a 61.5% return on invested capital and a gross yield of 6.8% in just three months.

If the growth period was indeed over, as they were led to believe, this kind of growth could not have happened. Aaron and Kira wouldn’t be out there right now, killing it in the real estate market.

Yet, they are. The couple is loving the way their whole life changed in less than a year since they started investing withDashdot. Fortunately, they listened to good advice, and have now changed the way they looked at property investing and what possible growth they could still have in the future.

While the growth period may still be going on, technically, the national boom has ended. As most people know, there was a “national property boom” and so it is easy to assume that all the growth happened during a finite period of time, and now that time has passed, it is all over.

However, what most people don’t realise is that “boom” only lasted for 7 months.

This is easy to define because in September 2020, the national median house price declined, and then in May 2021, we reached the peak of the growth rate, and the national median sales price growth rate has been declining since.

So, this allows us to understand two things.

1.The “boom” was not as long-lived as people think

2.Markets grew before, during, and after the national boom, once again proving that property markets are a local affair, not a national one.

Nevertheless, despite the fact that the national median sales price growth rate has been declining for some time, there are places where growth is still on the rise, as evidenced by Aaron and Kira’s story. As mentioned earlier, it’s simply a matter of buying at the right place at the right time.

Case in point:

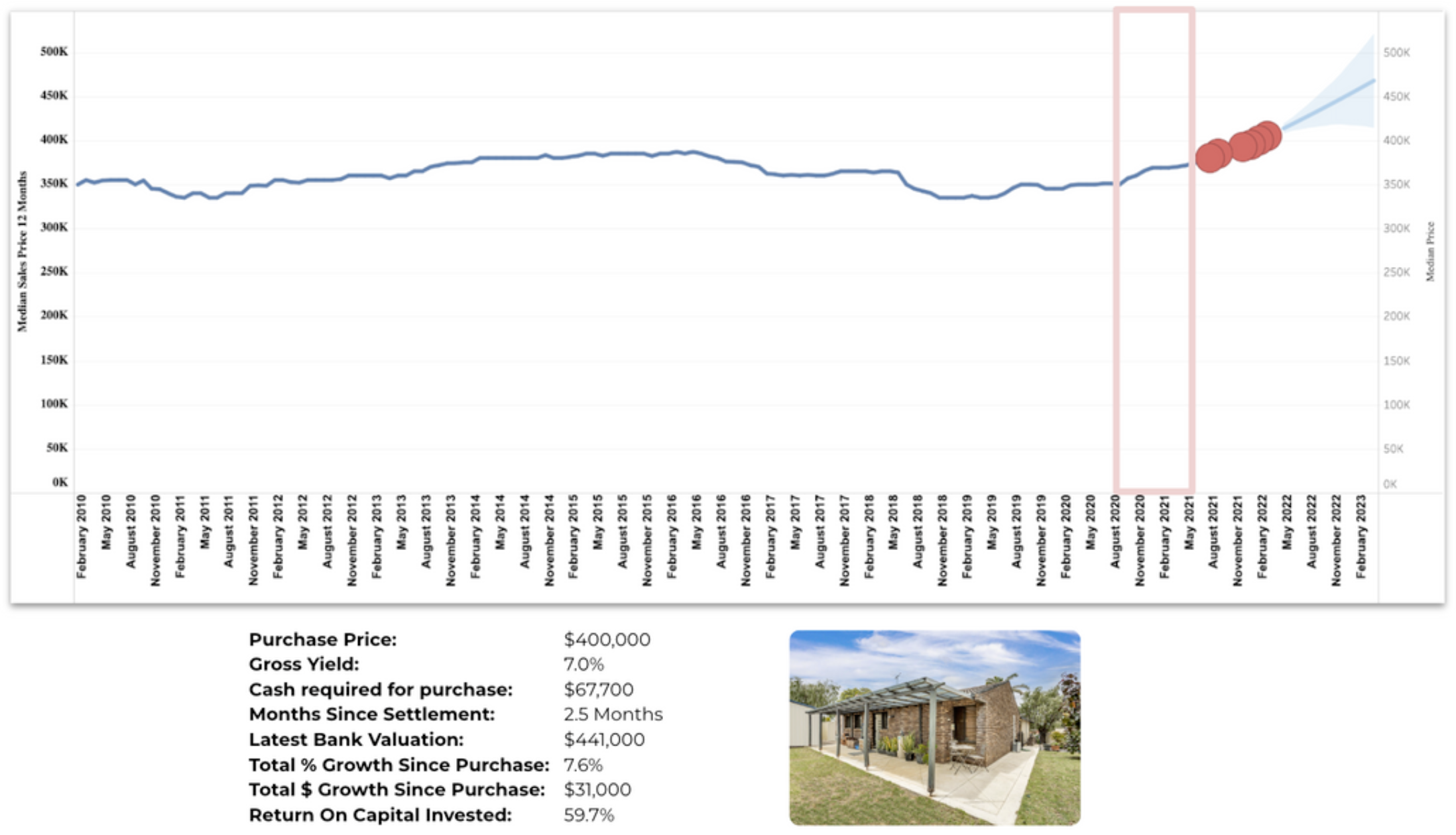

Goose & Gabi

Dashdot Location – Bought after the boom

Summed up above is an example of an investment we made AFTER the boom has ended.

Summed up above is an example of an investment we made AFTER the boom has ended.

Note how the market is still on the rise, but we managed to buy at a strategic time— as the area was just coming out of a trough.

We bought this property in the location property for $400,000.

And after two and a half months, it’s already shot up 7.6%, giving the owner a 59.7% return on invested capital.

While the boom has ended, look at what’s happening to this investment: the growth is still continuing. That’s because the growth is based on solid science and fundamentals.

The philosophy applied here is that investors should pick locations not based on what’s happening at the moment, but on where we project growth to be in the future. And we at Dashdot pride ourselves on entering markets before they start growing – whether that’s before, during, or after the so-called national boom has ended.

Conclusion: It’s Still a Good Time to Invest in Property, But Challenges Up Ahead

In reality, it’s getting challenging to find a property market that hasn’t had some growth from the boom that ended in 2021. After all, a staggering 90% of locations in Australia grew during this boom.

Still, we are of the opinion that just because a location has had growth doesn’t mean it’s all downhill from there. We firmly stand pat on our opinion that it is STILL a good time to invest in property.

In fact, a lot of places that we are buying right now have already seen some growth. We are confident about our prospects since we’re buying into locations that meet our holy trinity of strong fundamentals: lifestyle, jobs, and affordability.

Still, we have to admit that tough challenges are up ahead. The window of opportunity for experiencing life-changing growth in Australian real estate may still be wide open now, but it won’t stay like that forever.

Therefore, there is no time to waste for those who still wish to invest and earn big in property. There are still hundreds of locations out there waiting to be discovered before they finally join the fray of fully-grown- out areas.

It just bears reminding that for the property investors who are interested in searching and scaling those locations, it will take more than random lucky guesses and crossed fingers.

With the existing and future challenges to the property market, it will be a tough job to keep on finding these areas that are still up for long- term growth. This is why we’ve invested heavily into the science of what we’re doing.

In fact, we have developed the most advanced, scientific, property market research system in the country, which is why we’re able to continue to find the right property, in the right place, at the right time – no matter what is happening in the broader market.

So, if you want help to plan, growth, and manage your property portfolio, so you can achieve your life goals faster, and with much less risk – without worrying about market down turns, politics, or the economy – then reach to have a chat.

We pride ourselves on delivering a highly specialised, world-class service which is why we have an average 4.9 star review rating on Trustpilot and Google.

If that sounds like something you are interested in then book a call and have a chat with the team.

To your enduring success,

The Dashdot Team.