Executive Summary

Over the last 6 months, this is one of the most popular questions we’ve been getting here at Dashdot.

And to be honest, it’s a very legitimate question. After all, if the recent rate rises by the Reserve Bank of Australia (RBA) will affect your portfolio, you’d definitely want to know about it.

That’s why Dashdot’s Data & Technology team has conducted an exhaustive analysis on the interest rate effect, as well as a host of other variables. We did this to understand how your portfolio will potentially be affected in the coming years based on objective statistical measures.

In this article, we’ll dive into the past trends when it comes to interest rate rises, investigate what the data tell us about interest rates and property prices, and examine local and personal factors that can affect you and your portfolio.

The Link Between Interest Rates and Property Prices

In short: our analysis found that the correlation between interest rates and property growth was very weak.

And that means that interest rates just aren’t particularly important when looking to predict property prices.

In the not-so-short explanation of our findings, well, the data are very complex. See, we wanted to analyse a LOT of variables, not just interest rates. And the reason for that was to find out what other variables might have significant effects–even more significant than interest rates alone.

To do that, you’ll need an enormous amount of data. It’s because, for each additional variable, you’re increasing the amount of data you need exponentially. Otherwise, you’ll end up with a really loose, inaccurate model that doesn’t tell you much – particularly if your goal is to understand what is likely to happen in the future.

Fortunately, our number crunchers were up to the task. We were able to analyse – literally – millions of data points to work out the relationships between property prices and interest rates, as well as dozens of other variables.

And the results that we uncovered, quite frankly, will shock you.

Despite all the talk in the media about interest rates and how the ‘experts’ predicted they would affect property markets across Australia, we found barely any evidence of this happening historically at the state, city or regional level. Or of this happening at the moment.

But before we delve into the specifics of the data (which will be later in this report and ARE fascinating), we need to look at what correlation actually is…

…because, by and large, it’s one of the most misunderstood and misused terms you can find in all of statistics.

And you need to truly understand this to grow your property portfolio.

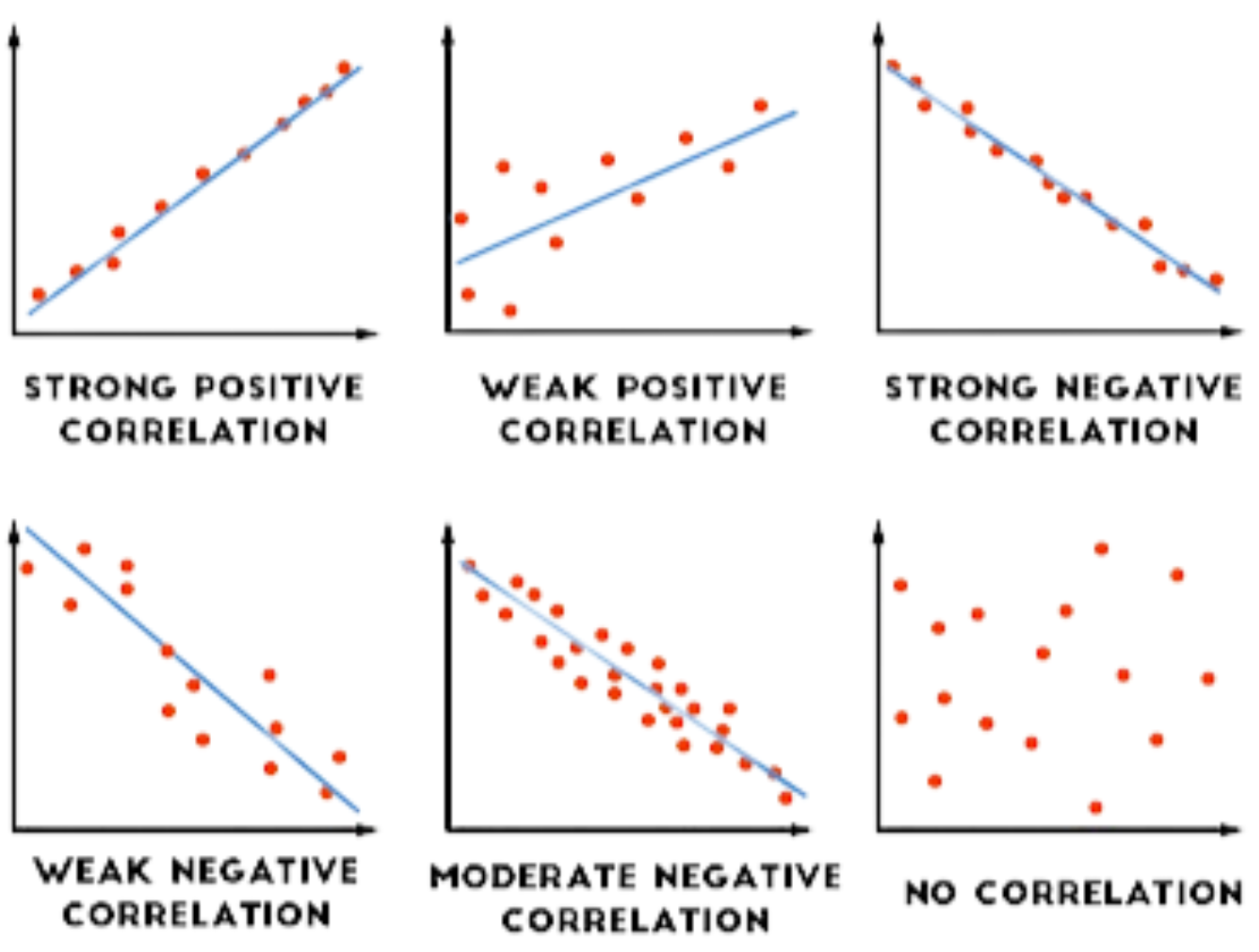

What is Correlation?

In technical terms, correlation tells us to which degree there is an observable co-movement between two variables.

In simple terms, correlation describes the degree to which two variables have historically moved in coordination with one another.

If data points between two variables are observed to move at the same time in the SAME direction consistently this is known as a ‘positive correlation’. The maximum positive correlation coefficient is 1.0 (i.e., 100% directional match in all observed data between the two variables every time).

If data points are observed to consistently move in the OPPOSITE direction, this is known as ‘negative correlation’. The maximum negative correlation coefficient is -1.0 (i.e., 100% inverse directional match in all observed data between the two variables every time).

If it seems that the data observed between the two variables is a little bit random and inconsistent, then it is somewhat intuitive to understand that there isn’t much of a relationship. This is known as ‘negligible correlation’ or ‘no correlation’. A negligible correlation coefficient is somewhere close to 0.0, either slightly above or below.

As an example, you could expect something like the number of left-foot shoes and the number of right-foot shoes sold per shoe store to have a very high positive correlation – approaching a perfect correlation of 1.0. But this is arguably not a very helpful correlation to really spend time and effort bother calculating in the first place.

For a more useful real-world example, think about if the population of a city increases. You would usually see food consumption in that city increase as well. In this case, you would expect to see a positive correlation. But it would not be expected to be a perfect correlation since different people eat different amounts of food, for example.

And if you were to find some data and plot these two variables (population and food consumption), you would probably find these two lines on the graph line moving up (as long as you adjust the scale). It’s because when the population goes up, food consumption follows really closely. And when the population decreases, food consumption goes down as well.

This point is a little tricky and is something that frequently causes confusion. The thing to note is that even though there is a decrease in each of these variables (i.e., a negative downward trend), this would still be a positive correlation as they still move in the same direction.

To give a more concrete example using data; here is a chart of a beach holiday town that has high seasonal fluctuations in population as people go on holiday here in the summer.

As the data points move in essentially the same direction at the same time with little variability in the relationship, a correlation of close to 1.0 would be expected to be observed and would be a ‘very high positive correlation’.

As the data points move in essentially the same direction at the same time with little variability in the relationship, a correlation of close to 1.0 would be expected to be observed and would be a ‘very high positive correlation’.

In the population vs. food consumption correlation analysis, there would be some variability in this relationship as different types, ages, and sizes of people eat different amounts. But it should still be expected that these data move with each other.

Now, in that example, it’s pretty clear and obvious that the additional population (variable A) is causing the increase in food consumption (variable B). That’s logical, and it’s also completely irrational for it to be the other way around. Variable B, food consumption, won’t cause an increase in population (variable A)

But that isn’t always the case when looking at two variables.

Sometimes, at first glance, it could look like A is causing B. But depending on the variables, it could actually be B causing A. In the case above, it is possible, though less likely, that food consumption (variable B) could cause population change (variable A), such as if there is something particularly delicious only available in the summer at a specific location. And that food causes people to travel there to consume it. Something like a specific time for summer tropical fruit harvests or a local seafood delicacy could lead to this dynamic in the data.

But there’s another possibility as well. It could be something that isn’t observable in the data for variable A, and variable B alone is causing this correlation.

Extending Our Understanding of Correlation to Causation

To explore this concept a little more deeply, we will look at some “studies” exploring the relationship between ice cream consumption and sunburn.

While we obviously aren’t talking about property here, the diagrams and concepts below will help you to visualise and understand more about Correlation vs. Causation.

In the diagram below, you can see that ice cream consumption is highly positively correlated with sunburn because the data points that make up the lines move so closely together at the same time.

Note: the data in this chart is aggregated annually.

With the results of a correlation analysis, you could likely conclude that there is a strong relationship between ice cream consumption and sunburns. From here, we can also hypothesise that this relationship will hold in the future.

In this chart, you can also see that over each subsequent year, there is an upwards trend between the variables. But what is driving this relationship?

This, importantly, is where we can investigate more variables to try to determine causation, which is what we’re really looking for.

So, what do you do?

Well, you could check if there was a population increase at the same time.

Your hypothesis could be that more people equals more ice cream and more sunburn in total.

So, rather than variable A affecting variable B – like in our food consumption and population example earlier – you investigate another variable C (population) affecting both variable A (ice cream consumption) and variable B (sunburns) in the same way.

You may then analyse the population data and find that the population didn’t increase but the amount of ice cream consumed per person increased. So, that analysis doesn’t explain the relationship between the two variables.

It could be that sunburn causes ice cream (I know, it sounds unlikely. But when checking for causation, it’s important to leave no stone unturned).

As an experiment to check the validity of this hypothesis, a good method might be to repeatedly lie in the sun until you get sunburned and wait for the ice cream to miraculously appear. And when it doesn’t, you can be fairly sure that sunburn doesn’t cause ice cream purchases.

Conversely, if you want to test whether ice cream causes sunburn, you could prevent sunburn by never eating ice cream again. So, you would NOT eat ice cream, but you’ll sit in the sun. And if you still get a sunburn, you have pretty compelling evidence that there is no causation between sunburn and ice cream.

Note that when testing those two hypotheses, I was describing a single person (you) getting sunburnt, or buying ice cream – that’s a sample size of 1.

But in reality, when testing a hypothesis, you need a much larger sample size. Nevertheless, if we make the very safe assumption that these two variables – buying ice cream and the risk of sunburns – are not, in fact, affecting one another…

…it means that there must be something else going on.

And that means we still need to identify what the true driver of this correlation is.

Before we go and find more data, however, we can further investigate using the data that we have. If we present the data in a different way, we may get closer to the truth.

In the chart below, you can see ice cream and sunburn charted out using the monthly aggregation data:

By using monthly data, you can see that there seems to be some sort of seasonal effect in play and that this is likely from a “study” conducted in the northern hemisphere. So, along with the monthly data, we can use weather data to analyse seasonal effects such as temperature (which was not possible to identify using the initial yearly analysis alone).

This may lead us to come up with the new hypothesis: that on sunny days, people are more likely to eat ice cream and get sunburned.

Funnily enough, property prices in Australia also have dramatic annual seasonal effects, which are not tied to interest rates, and can help with property price predictions. Perhaps your new hypothesis could be that sunny days make people more open to spending more money on property! And if that is your hypothesis, you would more than likely make a good scientist – you would be right according to the studies here and here.

The Dashdot D&T team always finds ways to dig deeper. Every piece of data and every research question asked brings us closer to the truth. The team is always looking at new ways to investigate slightly different research questions. This is part of the methodology that is used at Dashdot to build our predictive models and this approach is how we came up with the empirical results that determine the variables that truly drive property prices.

Okay, let’s go back to the main topic…

Recall that we were looking at the correlation between interest rates and property growth. And the reason we’re doing this is to help guide our research to determine if there’s any causation.

That’s because for investigating if there is likely to be any causal link between two variables, finding a strong correlation is a great thing to get started with.

(Yes, there are some cases where you can see a causal relationship without there being a correlation. But these are extremely rare and don’t apply in this case.)

So, a strong correlation would be our first indicator that there MIGHT be a causal link.

At Dashdot, our process is:

1. Investigate correlation;

2. IF there is a strong correlation, perform further data analysis to investigate this

phenomena to see if there are any causal links that can be established to help us better predict property prices.

Now, it is entirely possible, and certainly worth mentioning, that even if there is no causal link that can easily be explained, investigating correlation is still really important. After all, you don’t necessarily need to know what the cause is.

If interest rates and property growth move in a similar fashion time after time, year after year, you just need to know whether that is what happens, or not. And then, you’d want to know to what degree interest rates shift the needle.

Well, as I mentioned earlier, our analysis is that the link is generally weak.

Additionally, there are international economic forces that are empirically (and theoretically) tied to the decision-making process undertaken by the RBA when setting interest rates in Australia. These international economic forces are generally independent of the core drivers of property prices across Australia.

As soon as you start pulling on the thread of this concept, it gets tricky really quick. Luckily, Dashdot’s Data & Technology Team (D&T) team have enough data (and skills) to get really deep into what’s actually happening.

So buckle up. Here goes.

The first method of investigation that we undertook was measuring the historical correlation between a change in interest rates, and the average change in the Median Sale Price (MSP) of residential houses, particularly between January 2000 to July 2022.

This period was chosen because it had significant variability in interest rates and was a long enough period to provide enough data points without losing data quality.

So, what did the data and the empirical tests tell us?

Well, recall from earlier that a very strong positive correlation coefficient (close to 1.0) means that the changes observed for data points between two variables move up and/or down in the same direction at the same time, every time.

Additionally, a very strong negative correlation coefficient (close to -1.0) means that the observations of the data points between two variables move up and down in the opposite direction at the same time every time.

And a correlation coefficient close to 0.0 means that the data for the two variables essentially seems to be random vs. each other, and that there is no pattern to the relationship between them (based on the data in the data set).

The correlation that interest rates seem to have with changes in property prices at different rates and magnitudes in different parts of the country isn’t exactly zero, but it’s pretty close.

What’s also interesting is that the correlation between property prices and interest rates varies significantly by geographical area, and each area shows high variability over time, as seen in the figure below:

Interest Rate Changes and Property Price Changes : – Historical Correlation Coefficients by Capital City and Rest of State

So, can we rely on interest rates as an indicator for expected individual property price changes in different parts of Australia in the future?

Hell no!

In fact, the interest rate is such a poor lead indicator of property prices that it isn’t even in the top 50 core features in our predictive model for property prices, or predictive model for rental prices, which we have applied to compare every Australian suburb (where there is enough available, reliable data for modelling purposes).

Back to Correlation and Causation – From Ice-Cream to Property Prices

After measuring the correlation between two variables, even if the relationship is weak,, the next question is; how much does this matter?

Correlation alone is not enough to establish if a change in interest rate can be causally attributed as the primary driver of property price changes.

While correlation analysis helps researchers to identify if something is going on, it cannot tell us everything about what is going on under the hood.

Correlation studies help us to figure out how to explore this relationship further and can help to guide the direction of future experiments based on these results.

Ultimately though, we are looking for a causal relationship. It’s because we want consistent, predictive power that we can rely on across time and geographies.

We want to know if a change in one variable will allow us to predict a change in the variable of interest – in this case, property prices.

To tie this back in with our initial example on correlation, here is our ice-cream sunburn correlation, along with a friendly causal sun representing the initially unobserved causal variable leading to the observed correlation.

To translate the diagram above into the property price prediction correlations analogy, all we need to do is change the word ice cream to interest rates and median sales price to sunburn. Then, we put our science hats back on and go digging for all of the unobserved causal drivers of this relationship until we can explain it using data in a way that has high predictive power.

What Our Clients Really Want to Know

We researched the historical, and current, interest rates set by the RBA and found that this is not the primary driver of property price changes for suburbs in every state across Australia.

Interest rate decisions by the RBA are unique in their historical context and only matter as the primary driver in some suburbs. But only some of the time over different periods, and with different levels of predictive power.

At this point, it is probably worth highlighting that the answer to the “interest rates” question is not what our clients really want to know.

And this brings us to the core reason why Dashdot exists in the first place.

In essence, our conversations around property investment and interest rates are not really aimed at engaging in a technical discussion about our methodological, theoretical, or empirical macroeconomic approach.

Nor are our clients highly motivated to enter a discussion around quantifying the responsiveness of national property prices to corresponding policy changes by the RBA.

Our clients are seeking answers to different questions. In spite of the great risk of paraphrasing, the answer that property investors are seeking is more of a response to the question:

“Will I lose money and bankrupt my family if I buy an investment property now and the price goes down?”

“Should I wait until there are different market conditions with less risk of prices going down?”

Are these valid questions? Absolutely!

But broadly speaking, these questions both fall under the core umbrella question that we are going to address directly:

“Saving this money took me years of blood, sweat and tears. So, how do I know if I should buy what you are selling there, Mr. Dashdot?”

The answer to each of these questions is more related to the personal circumstances of the individual(s) asking the question. And the correct answer is directly related to delivering specific individual advice on how to make the best decision now so that they can work out the best plan to reach their financial and personal goals in the future.

The degree to which investment property price fluctuations and net cash flow fluctuations can be tolerated by individuals depends on their individual financial position, stability of income, future spending plans and personal risk preference.

So, one question that should be asked in this regard is:

“If every individual has a different financial position, are all investments the right one for every individual, in every circumstance at every time?”

The answer to this question is really easy: No.

It should be fairly obvious that every property investment will not be right for every individual in every circumstance at every time.

So, should you buy property in a rising interest rates environment? The answer to this varies by individual, individual preferences, and individual financial circumstances.

And yes, interest rate rises will lead to price decline in some properties in some parts of Australia. But this is not the major price driver.

What needs to be understood at this point is that interest rates are simply not the most impactful driver of property prices in nearly every part of the country today. Nor has it been at any other point in Australia’s property market history, according to the wealth of data that the Dashdot D&T team has looked at.

Additionally worth mentioning on a technical note is that the relationship between changes in interest rates and property prices is typically compared to the impact on the ‘average’ property price.

You can’t tell from this average number if more big houses or small houses were sold from this aggregated number. So, you would need more data to get a more meaningful interpretation from this analysis.

And even if you were in charge of a truly massive portfolio (which more closely resembles the “average”), then this slight decline in a minor part of your portfolio may be your fate for some number of months into the future due to interest rate changes. But even then, it would likely be a transitory effect on your net wealth position.

So, when considering how interest rate rises will affect your decisions, it comes down to honestly evaluating your personal circumstances.

You are not an “average” – you are unique.

That’s why when considering property investments, you don’t really need to pay attention to the averages of some macroeconomic metric. Instead, you need to care about trying to quantify the impact of tangible and intangible risks on your personal financial situation.

And how much money you may lose or gain on any property investment depends on: Which property you buy

The risks associated with where it is located

What the likely rental return is

What the holding costs of the property are

Whether or not your personal situation may force you to sell in a depressed market

So, the RBA’s interest rate policy has a negligible correlation with property prices in most parts of the country.

What you should be aware of is that the RBA interest rate policy will definitely have an effect on the overall economy. And those macroeconomic metrics, such as unemployment, inflation and wage growth in different industries, may impact your personal economic circumstances.

This could hinder your ability to service the variable costs of your investments. So, while RBA decisions may have a very minor effect on property prices, the main factor to consider is how you manage the risks associated with your personal economic circumstances.

With that in mind, the question surrounding interest rates initially posited is dramatically different to the answer to the question that property investors like you really want to know, which is:

“Will I lose money and bankrupt my family if I buy an investment property now?”

The answer to this question today, tomorrow, and across almost every period in the history of the Australian property market is:

Almost certainly not.

Property prices have a tendency towards positive returns across time and different regions of the country – with different spikes in local prices caused by different drivers at different times.

If you still want to learn some more about how interest rates work and how they impact the Australian economy (as well as your personal economy), read on! If that all seems like a lot of work with a steep learning curve, that’s because it is.

The RBA, the Economy and You

To make it clear from the outset, it isn’t really a surprise that interest rates set by the RBA do not have a hugely significant correlation with property prices in Australia. The RBA does not have the mandate to try to control property prices.

Changes in interest rates are a blunt national level, an aggregate tool to help stimulate or cool the economy overall. The setting of interest rates is specifically used as one of the policy levers that can be pulled to keep measures of inflation within a mid-term range of 2-3%.

Inflation seems like a vague businessman or banker kind of word. But what it really means is the aggregate change in prices.

If inflation has gone up, your paycheck will buy roughly that proportion fewer goods. If inflation has gone down, it means your salary will buy more goods.

But the tricky bit is that how much money consumers have in their pockets determines roughly how much prices will go up and down.

So, it is a moving target, with simultaneously changing policies that impact each other in an iterative back-and-forth way. That is to say, understanding the impact that interest rates will have on property prices is complicated.

While the RBA may take into account the impact of interest rates on property markets, other indicators such as employment levels, wages, credit markets, financial stability, and the value of the currency are what really drive their decisions when setting interest rates. Local effects from interest rate changes are likely to be from different drivers in every local economy, every local labour market and the decisions that drive local buyers (or external investors) to buy and/or sell property. These varied decisions aggregated are what form the change in property prices.

RBA Cash Interest Rate Target

To navigate through the COVID-19 pandemic, the RBA took to lower interest rates to ‘emergency historic low levels’ of 0.1%’ – a decision they made for the first time.

And after three years, we’ve now had seven rises in seven months.

With Russia’s invasion of Ukraine, corresponding increase in energy prices and wider geopolitical risk, interest rate decisions are now being driven by both changes in the domestic economy and the international macroeconomic forces impacting the cost of living in Australia.

The question surrounding RBA interest rate decisions by the board is no longer centred around helping mitigate the shock of a once-in-a-lifetime global pandemic, but rather on the brave new world of spiralling inflation, global geopolitical tension and a rental market crisis (RBA Statement of Monetary Policy August 2022).

This difference in situation is vitally important to understand, as keeping inflation within 2-3% per annum is the core target of RBA monetary policy that must be followed in line with the current Objectives of RBA Monetary Policy.

Interest rates have gone up, and this has very recently coincided with a minorly correlated decrease in average property prices across the nation that were sold over this period. The question now, given that Australia is in a new domestic and international economic environment, is how high and how fast will interest rates change.

The RBA’s decision will come to define how the economy of Australia develops. However, this should not be expected to be the primary driver of property prices today or tomorrow, and generally in most places in Australia.

While the change in the official RBA interest rates is frequently discussed around dinner tables, at pubs, and in the news cycles, frequently missing are the other ‘non- interest rate’ changes in RBA policies that should be part of the discussion.

Most homeowners in Australia are likely not aware that the RBA has significant policy levers outside of changing the interest rate that impacts the Australian economy, the stability of financial & banking systems, the unemployment and wage rate, as well as the value of the Australian Dollar.

It is also not well known that these policies impact property prices across the country differentially. And that there are also interaction effects between these variables and interest rates all happening at the same time.

So, property investors in Australia should attempt to take the direct, indirect, and interactive effects of these RBA policies into account when making decisions impacting:

- What they buy

- Where they live

- Whether they have more children

- Which employment opportunities to take

- Whether to study to gather new skills to enter the economy of the future

- Whether or not to ask for a raise

- If, how, when and where you should buy or sell an investment property

It seems likely that the majority of property price decisions to be taken by individuals and families will NOT be done after such a complex analysis.

In practice, different people are at different stages in life, with different jobs, in different personal circumstances, and in different parts of the country. As a result, each has different local economic drivers that will change their behaviour at different rates in response to their individual circumstances. Whatever drives their decision, it is gloriously unlikely to be primarily in direct response to RBA monetary policies.

Uncovering The Key Drivers of Property Prices

At Dashdot, our purpose is to provide the answers to the questions surrounding informed choices in property investment. Obviously, interest rates are a hot topic now the RBA seems poised for more rises. We hope that this article has helped you cut through some of the hype and noise surrounding investing in the Australian property market.

In the forthcoming series of research papers by Dashdot, we will articulate some of the key drivers of property prices in the future.

We will explain how we use the vast amount of data that Dashdot has to ask the questions that most property owners haven’t even thought of. We will also explain how we have turned this data into empirically-verified indicators to feed into our price prediction modelling infrastructure to provide the data-driven answers to help you pick the right property, in the right place, at the right time.

Want to know more? Click here to have a friendly chat with the Dashdot team and we will break down everything that you need to know to maximise returns for your new property portfolio.